Financial accounting is a specialized branch of accounting that keeps track of a company's financial transactions. Using standardized guidelines, the transactions are recorded, summarized, and presented in a financial report or financial statement such as an income statement or a balance sheet.

Companies issue financial statements on a routine schedule. The statements are considered external because they are given to people outside of the company, with the primary recipients being owners/stockholders, as well as certain lenders. If a corporation's stock is publicly traded, however, its financial statements (and other financial reportings) tend to be widely circulated, and information will likely reach secondary recipients such as competitors, customers, employees, labor organizations, and investment analysts.

It's important to point out that the purpose of financial accounting is not to report the value of a company. Rather, its purpose is to provide enough information for others to assess the value of a company for themselves.

Because external financial statements are used by a variety of people in a variety of ways, financial accounting has common rules known asaccounting standards and as generally accepted accounting principles (GAAP). In the U.S., the Financial Accounting Standards Board (FASB) is the organization that develops the accounting standards and principles. Corporations whose stock is publicly traded must also comply with the reporting requirements of the Securities and Exchange Commission (SEC), an agency of the U.S. government.

Double Entry and the Accrual Basis of Accounting

At the heart of financial accounting is the system known as double entry bookkeeping (or "double entry accounting"). Each financial transaction that a company makes is recorded by using this system.

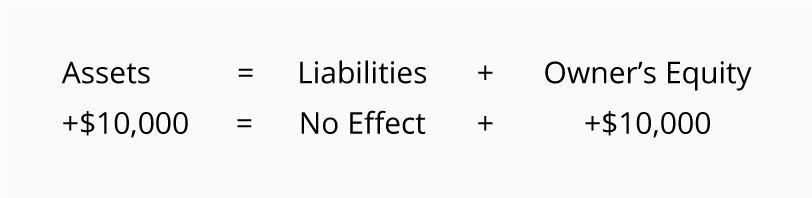

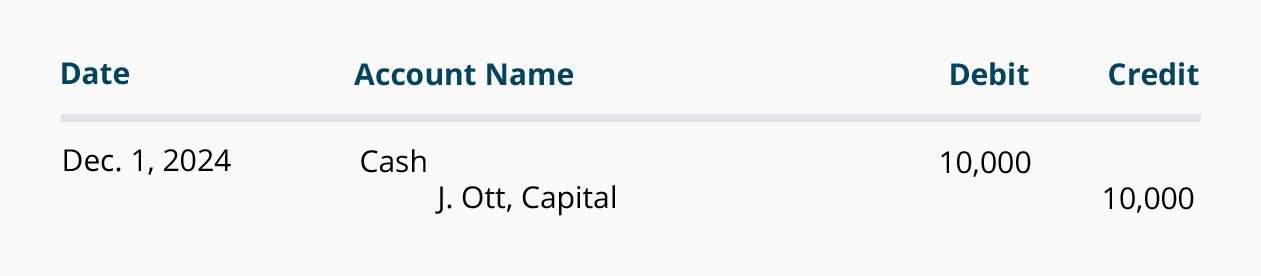

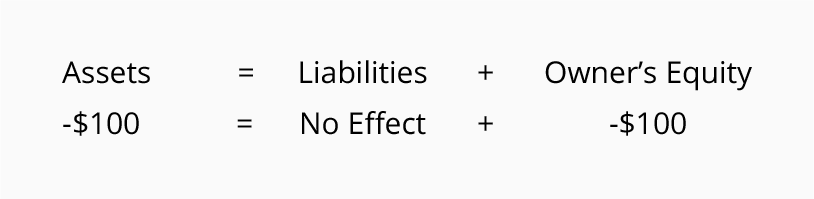

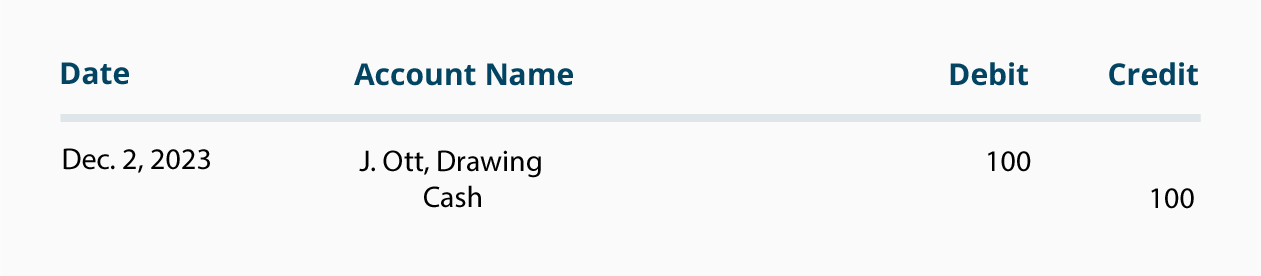

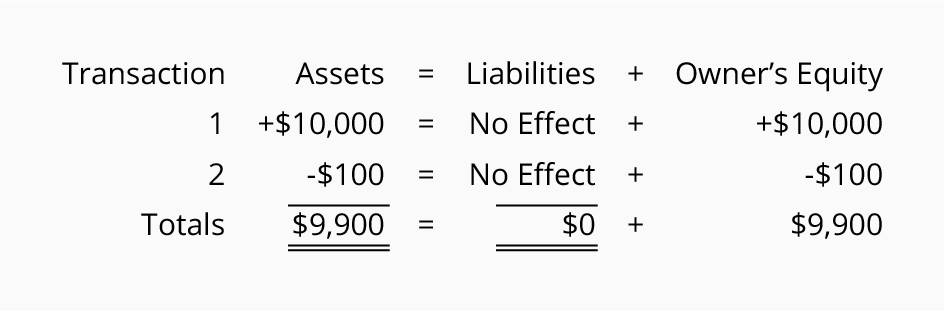

The term "double entry" means that every transaction affects at least two accounts. For example, if a company borrows $50,000 from its bank, the company's

Cash account increases, and the company's

Notes Payable account increases. Double entry also means that one of the accounts must have an amount entered as a

debit, and one of the accounts must have an amount entered as a

credit. For any given transaction, the debit amount must equal the credit amount. (To learn more about debits and credits, see

Explanation of Debits & Credits.)

The advantage of double entry accounting is this: at any given time, the balance of a company's asset accounts will equal the balance of its liability and stockholders' (or owner's) equity accounts. (To learn more on how this equality is maintained, see the

Explanation of Accounting Equation.)

Financial accounting is required to follow the

accrual basis of accounting (as opposed to the "cash basis" of accounting). Under the accrual basis, revenues are reported when they are

earned, not when the money is received. Similarly, expenses are reported when they are

incurred, not when they are paid. For example, although a magazine publisher receives a $24 check from a customer for an annual subscription, the publisher reports as revenue a monthly amount of $2 (one-twelfth of the annual subscription amount). In the same way, it reports its property tax expense each month as one-twelfth of the annual property tax bill.

By following the accrual basis of accounting, a company's profitability, assets, liabilities and other financial information is more in line with economic reality. (To learn more on achieving the accrual basis of accounting, see the

Explanation of Adjusting Entries.)

Accounting Principles

If financial accounting is going to be useful, a company's reports need to be credible, easy to understand, and comparable to those of other companies. To this end, financial accounting follows a set of common rules known as accounting standards or generally accepted accounting principles (GAAP, pronounced "gap").

GAAP is based on some basic underlying principles and concepts such as the cost principle, matching principle, full disclosure, going concern, economic entity, conservatism, relevance, and reliability. (You can learn more about the basic principles in

Explanation of Accounting Principles.)

GAAP, however, is not static. It includes some very complex standards that were issued in response to some very complicated business transactions. GAAP also addresses accounting practices that may be unique to particular industries, such as utility, banking, and insurance. Often these practices are a response to changes in government regulations of the industry.

GAAP includes many specific pronouncements as issued by the Financial Accounting Standards Board (FASB, pronounced "fas-bee"). The FASB is a non-government group that researches current needs and develops accounting rules to meet those needs. (You can learn more about FASB and its accounting pronouncements at

www.FASB.org.)

In addition to following the provisions of GAAP, any corporation whose stock is publicly traded is also subject to the reporting requirements of the Securities and Exchange Commission (SEC), an agency of the U.S. government. These requirements mandate an annual report to stockholders as well as an annual report to the SEC. The annual report to the SEC requires that independent certified public accountants audit a company's financial statements, thus giving assurance that the company has followed GAAP.

Financial Statements

Financial accounting generates the following general-purpose, external, financial statements:

- Income statement (sometimes referred to as "results of operations" or "earnings statement" or "profit and loss [P&L] statement")

- Balance sheet (sometimes referred to as "statement of financial position")

- Statement of cash flows (sometimes referred to as "cash flow statement")

- Statement of stockholders' equity

Income Statement

The income statement reports a company's profitability during a specified period of time. The period of time could be one year, one month, three months, 13 weeks, or any other time interval chosen by the company.

The main components of the income statement are revenues, expenses, gains, and losses. Revenues include such things as sales, service revenues, and interest revenue. Expenses include the cost of goods sold, operating expenses (such as salaries, rent, utilities, advertising), and nonoperating expenses (such as interest expense). If a corporation's stock is publicly traded, the earnings per share of its common stock are reported on the income statement. (You can learn more about the income statement at

Explanation of Income Statement.)

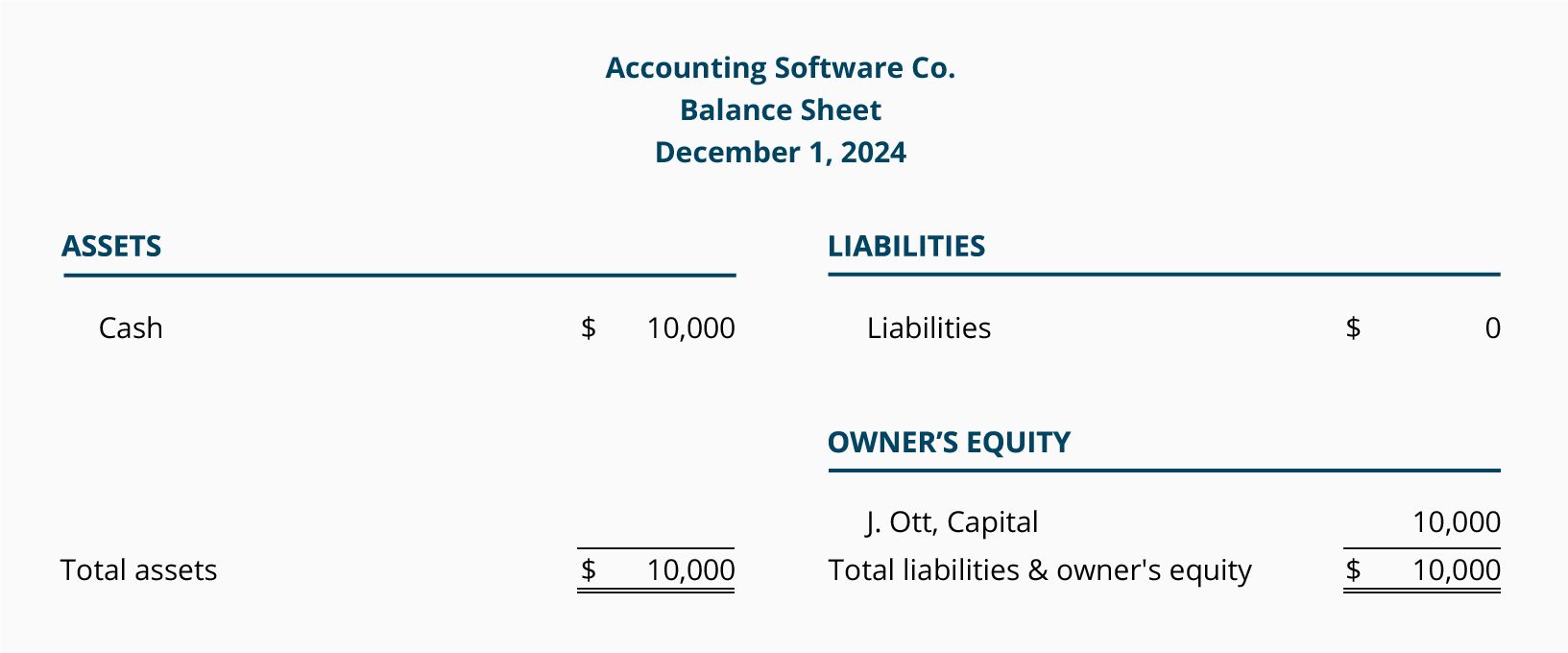

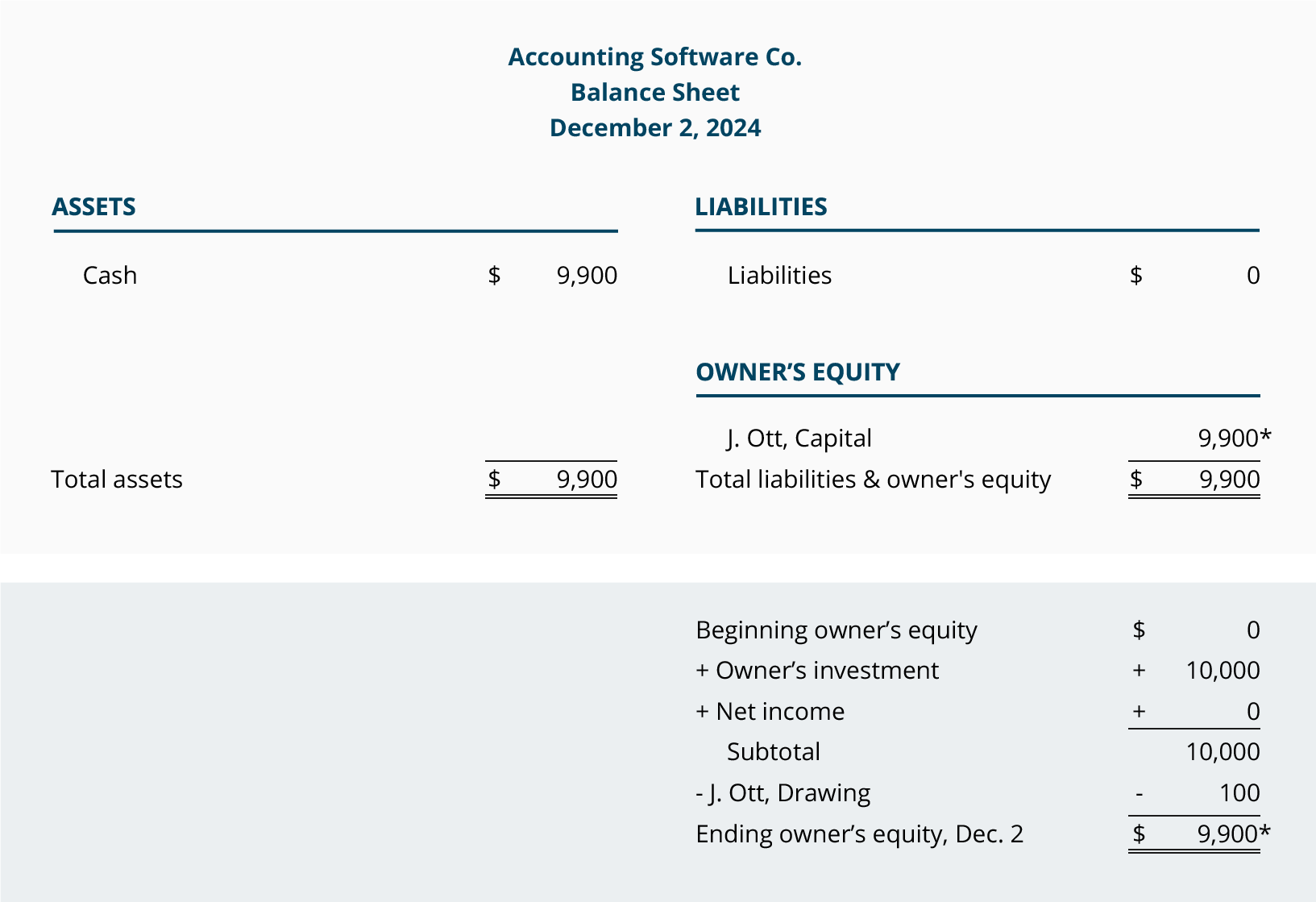

Balance Sheet

The balance sheet is organized into three parts: (1) assets, (2) liabilities, and (3) stockholders' equity at a specified date (typically, this date is the last day of an accounting period).

The first section of the balance sheet reports the company's

assets and includes such things as cash, accounts receivable, inventory, prepaid insurance, buildings, and equipment. The next section reports the company's

liabilities; these are obligations that are due at the date of the balance sheet and often include the word "payable" in their title (Notes Payable, Accounts Payable, Wages Payable, and Interest Payable). The final section is

stockholders' equity, defined as the difference between the amount of assets and the amount of liabilities. (You can learn more about the balance sheet at

Explanation of Balance Sheet.)

Statement of Cash Flows

The statement of cash flows explains the change in a company's cash (and cash equivalents) during the time interval indicated in the heading of the statement. The change is divided into three parts: (1) operating activities, (2) investing activities, and (3) financing activities.

The

operating activities section explains how a company's cash (and cash equivalents) have changed due to operations.

Investing activities refer to amounts spent or received in transactions involving long-term assets. The

financing activities section reports such things as cash received through the issuance of long-term debt, the issuance of stock, or money spent to retire long-term liabilities. (You can learn more about the statement of cash flows at

Explanation of Cash Flow Statement.)

Statement of Stockholders' Equity

The statement of stockholders' (or shareholders') equity lists the changes in stockholders' equity for the same period as the income statement and the cash flow statement. The changes will include items such as net income, other comprehensive income, dividends, the repurchase of common stock, and the exercise of stock options.

Financial Reporting

Financial reporting is a broader concept than financial statements. In addition to the financial statements, financial reporting includes the company's annual report to stockholders, its annual report to the Securities and Exchange Commission (Form 10-K), its proxy statement, and other financial information reported by the company.

Financial Accounting vs. "Other" Accounting

Financial accounting represents just one sector in the field of business accounting. Another sector, managerial accounting, is so named because it provides financial information to a company's management. This information is generally internal (not distributed outside of the company) and is primarily used by management to make decisions. Other sectors of the accounting field include cost accounting, tax accounting, and auditing.

There are a wide range of career opportunities for accounting graduates and understanding your interests and strengths can help you choose a good fit for you. You can pursue work as an accountant at a corporation or non-profit, accounting firm, the government, or start your own practice. The largest accounting firms, known as the Big Four, are large recruiters of new accounting graduates and were all named to Fortune Magazine’s list of the 100 Best Companies to Work For for 2012. The Big Four includes Deloitte & Touche, Ernst & Young, KPMG, and PricewaterhouseCoopers. Government agencies like the FBI and IRS are large employers of accountants who work to investigate fraud and other illegal financial activities. For individuals who like the freedom and flexibility of being your own boss, starting your own accounting business can be a great option.'

There are a wide range of career opportunities for accounting graduates and understanding your interests and strengths can help you choose a good fit for you. You can pursue work as an accountant at a corporation or non-profit, accounting firm, the government, or start your own practice. The largest accounting firms, known as the Big Four, are large recruiters of new accounting graduates and were all named to Fortune Magazine’s list of the 100 Best Companies to Work For for 2012. The Big Four includes Deloitte & Touche, Ernst & Young, KPMG, and PricewaterhouseCoopers. Government agencies like the FBI and IRS are large employers of accountants who work to investigate fraud and other illegal financial activities. For individuals who like the freedom and flexibility of being your own boss, starting your own accounting business can be a great option.'